Strategic Growth Examples

These examples are designed to help you understand how an Indexed Universal Life (IUL) policy may support long-term protection and potential cash value accumulation. The goal is to give you an educational look at how an IUL strategy can be structured, not predict or guarantee performance. Actual policy values and outcomes will vary based on state of issue, age, health, underwriting class, product design, index allocation, and carrier-specific guidelines.

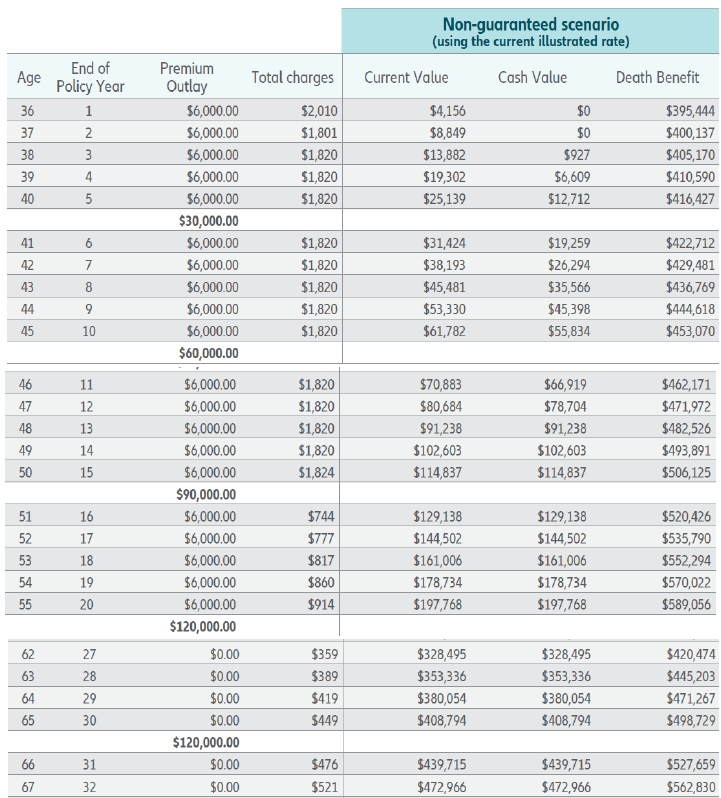

Non-guaranteed Example Scenario (educational purposes only)*

$500/month premium for 20 years only

Increasing Life Insurance Death Benefit

6.65% Illustrative Rate

Balanced index allocation (examples may include equity indices and multi-asset strategies)

At Retirement Age 67 (these values are hypothetical and for educational use only)*

Structured for 20 years of premium Contributions

Illustrative Cash Value (hypothetical): $472,966

Illustrative Death benefit (hypothetical): $562,830

Goals

Long-term life insurance protection for family

Potential tax-advantaged cash value growth

Flexibility for future financial needs: child’s college, home

Ability to access tax-advantaged cash value during her lifetime for her child’s new business venture, house down payment and to supplement some of her retirement income*

Meet Sarah, 35 years old*

Non-guaranteed Example Scenario (educational purposes only)*

$500/month premium for 20 years only

Increasing Life Insurance Death Benefit

6.65% Illustrative Rate

Balanced index allocation (examples may include equity indices and multi-asset strategies)

At Retirement Age 67 (these values are hypothetical and for educational use only)*

Structured for 20 years of premium contributions

Illustration Cash Value (hypothetical): $426,478

Illustrative Death benefit (hypothetical): $507,509

Goals

Long-term life insurance protection for family

Potential tax-advantaged cash value growth

Ability to access tax-advantaged cash value during his lifetime through policy loans for his child’s college tuition, house down payment and to supplement some of his retirement income*

Meet John, 36 years old*

Sarah & John purchase an IUL policy on their 3 year old child, Avery*

Non-guaranteed Example Scenario (educational purposes only)*

John & Sarah purchase an IUL policy on Avery at age 3

$300/month premium for 20 years only

Increasing Death Benefit

6.65% Illustrative Rate

Balanced index allocation (examples may include equity indices and multi-asset strategies)

Goals for their child, Avery’s policy

Guaranteed insurability at an early age: Children can be insured as early as 14 days old in California.

Long-Term tax-advantaged cash value growth: The policy can accumulate cash value over your child’s lifetime., compounding more efficiently on a tax deferred basis.

Future transfer and generational wealth: Ownership of the policy can be transferred to the child later in life, allowing it to serve as a gift, inheritance, or foundational financial asset.

Access to cash value later in life: Your child can can use the policy’s cash value through loans or withdrawals for future needs such as education, a first home, family expenses or retirement. (Loans and withdrawals reduce cash value and death benefit)

If the policy is untouched until 60 years old (these values are hypothetical and for educational use only)*

Illustrative Cash Value (hypothetical): $1,768,118

Illustrative Death benefit (hypothetical): $2,369,279

*Disclosure: This material is for educational purposes only and is intended to provide a general overview of the life insurance concepts and product features discussed. Sample Indexed Universal Life (IUL) scenarios are hypothetical and for illustration purposes only. Actual IUL policy features and values vary based residential state, age, health, underwriting, and carrier-specific guidelines.

Policy benefits, guarantees, charges, and performance vary by carrier and by individual policy design. Nothing presented here should be interpreted as personalized financial, tax, or legal advice.

To understand which life insurance options may be appropriate for your specific goals, please contact us fir a personalized review and customized strategy.